For related reading, see our guide on dental practice growth strategies.

Reducing dental insurance dependence is the single most consequential financial decision a practice owner can make. When PPO reimbursements cover 40–60 cents on every dollar of your standard fee — and write-offs consume an average of 30–45% of production annually (ADA Health Policy Institute, 2023) — the math is not sustainable long-term. The practices that have successfully reduced insurance dependency — some dropping from 90% insured to under 40% over three to five years — consistently report higher net income, fewer administrative headaches, and stronger patient relationships. This guide shows you exactly how to do it.

For related reading, see our guide on improving dental practice profitability.

For related reading, see our guide on dental insurance credentialing guide.

For related reading, see our guide on explaining insurance changes to patients.

For related reading, see our guide on long-term financial stability after dropping PPOs.

For related reading, see our guide on creating a dental membership plan.

For related reading, see our guide on PPO transition success stories.

For related reading, see our guide on negotiating better dental insurance rates.

For related reading, see our guide on managing PPO plan risks.

TL;DR — Key Takeaways

- Most PPO-heavy practices write off 30–45% of production annually — this is the core financial problem insurance exposure creates.

- The transition is a multi-year process: practices that try to drop all PPOs simultaneously lose patients and revenue; those that phase down over 3–5 years typically retain 70–85% of their patient base.

- In-house membership plans are the most effective single tool for replacing insured patients with loyal, cash-paying ones — with annual memberships averaging $300–$500 per patient.

- PPO contract negotiation is underused: fewer than 20% of dentists regularly negotiate fee schedules (ADA Center for Professional Success, 2024), yet targeted negotiations can recover 5–15% on key procedure codes.

- Patient communication is the make-or-break variable — practices with a scripted, empathetic changeover conversation retain far more patients than those that simply announce policy changes.

How Does PPO Dependency Affect Your Dental Practice Financially?

Insurance dependency, in the context of dental practice management, refers to a revenue structure where the majority of your collections flow through third-party payer contracts — primarily PPO networks. A practice is usually considered heavily insurance-dependent when more than 60–70% of its patient base carries PPO insurance and expects you to accept the negotiated (reduced) fee schedule.

The distinction matters because PPO participation is not simply “accepting insurance.” It is an agreement to discount every procedure in your fee schedule by a percentage determined by the insurer, not you. When you sign a PPO contract, you agree to write off the difference between your standard fee and the plan’s allowed amount. For high-overhead procedures like crowns, implants, or full-mouth restorations, that write-off can exceed $300–$600 per case.

This model made strategic sense in the 1990s and early 2000s, when PPO reimbursements tracked closer to actual costs and the network drove meaningful new patient volume. That dynamic has shifted substantially. According to the American Dental Association’s Health Policy Institute [1], real PPO reimbursement rates have declined in inflation-adjusted terms over the past two decades, even as practice operating costs — staff wages, supplies, equipment, facility costs — have risen sharply. The ADA’s 2023 Dentist Income Survey found that practice expenses as a percentage of collections have increased significantly for solo and small-group practices, with insurance administrative overhead identified as one of the primary drivers.

Understanding PPO dependence also means recognizing what it costs beyond the write-off: billing staff time processing claims, re-filing denials, chasing authorizations, appealing downgrades, and managing the accounts receivable aging that comes with 30–45 day reimbursement cycles. For a practice doing $1.2M in production annually with a 35% PPO write-off rate, the actual collected revenue is closer to $780,000 — before overhead. Reducing that write-off rate by 10 percentage points would recover $120,000 in annual collections with zero additional clinical work.

That is the core argument for reducing insurance dependency: not that insurance is inherently wrong, but that unchecked PPO reliance structurally caps your income and limits your clinical autonomy. The goal of this guide is to show you a measured, patient-centered path toward a healthier revenue mix.

Signs Your Practice Is Over-Dependent on Insurance

Over-exposure on insurance doesn’t always feel like a crisis. It often feels like a busy practice — full schedule, high production, active patient base. The problem surfaces in your bank account, not your appointment book. Here are the concrete indicators that your practice has crossed into problematic PPO dependency:

1. Your Collections Consistently Fall 30–45% Below Production

Production is what you do. Collections is what you keep. If your practice consistently produces $100,000/month but collects $60,000–$70,000, the gap is largely attributable to PPO write-offs. A healthy practice should be collecting 95–98% of adjusted production (production after write-offs). If your collection rate looks strong but your net income feels thin, the problem is in the write-off volume, not collections efficiency.

2. You Haven’t Raised Your Fee Schedule in 2+ Years

PPO participation often creates a psychological barrier to raising fees. Dentists in heavy PPO practices sometimes avoid updating their fee schedule because they believe it doesn’t matter — the PPO will dictate what they collect anyway. This is partially true for in-network procedures, but your fee schedule matters for non-covered services, cosmetic cases, and as use during PPO fee negotiations. Stagnant fee schedules are a sign that the PPO relationship has inverted: instead of you setting the price, the insurer has effectively done it for you.

3. Your New Patient Pipeline Requires Insurance Acceptance

When new patients ask “Do you take my insurance?” as the first question and you’ve built your marketing around “We accept most PPOs,” your practice growth has become insurance-dependent by design. Contrast this with practices that attract new patients based on outcomes, technology, comfort, or a specific patient experience — those practices convert a far higher percentage of uninsured or out-of-network patients.

4. Your Administrative Team Spends More Than 10% of Hours on Insurance

A reasonable benchmark for insurance-related administrative time is 5–8% of total front-office hours for a moderately insured practice. If your front desk or billing coordinator is spending 15–25% of their week on claims, authorizations, appeals, and insurance calls, you have an operational dependency problem. The National Association of Dental Plans (NADP) [2] has documented that the average dental claim requires 2.4 administrative touchpoints before final resolution — a figure that increases with claim complexity and downcoding frequency.

5. You Feel Unable to Recommend Your Best Treatment Options

This is the clinical sign of overdependence, and it’s the one that dental school never prepares you for. When a patient’s insurance doesn’t cover a particular procedure or material, and you find yourself recommending the covered alternative rather than the clinically optimal one, insurance has entered your clinical decision-making. This is a patient care problem as much as a financial one.

6. Your Case Acceptance Rate for Non-Covered Services is Below 40%

In a practice where patients expect insurance to pay for everything, case acceptance for non-covered or elective procedures commonly hovers in the 30–40% range. In fee-for-service or membership-plan practices, case acceptance for the same procedures regularly exceeds 65–75%, because patients have already made a value-based commitment to the practice rather than to their plan benefits.

What Is the Real Financial Impact of PPO Dependence?

The financial case for reducing dental insurance exposure becomes clear when you quantify the specific cost categories that PPO participation creates. Most practice owners underestimate the true cost because it’s distributed across multiple line items rather than appearing as a single “insurance expense.”

The Write-Off Problem

The most direct cost is the write-off: the difference between your standard fee and the PPO’s contracted allowed amount. According to data compiled by Dental Economics [3], the average PPO discount across major procedure categories ranges from 20% to 55%, with higher-value restorative and prosthetic codes experiencing the steepest reductions. A crown that you charge $1,400 may reimburse at $800–$900 under a major PPO plan — a write-off of $500 or more per unit.

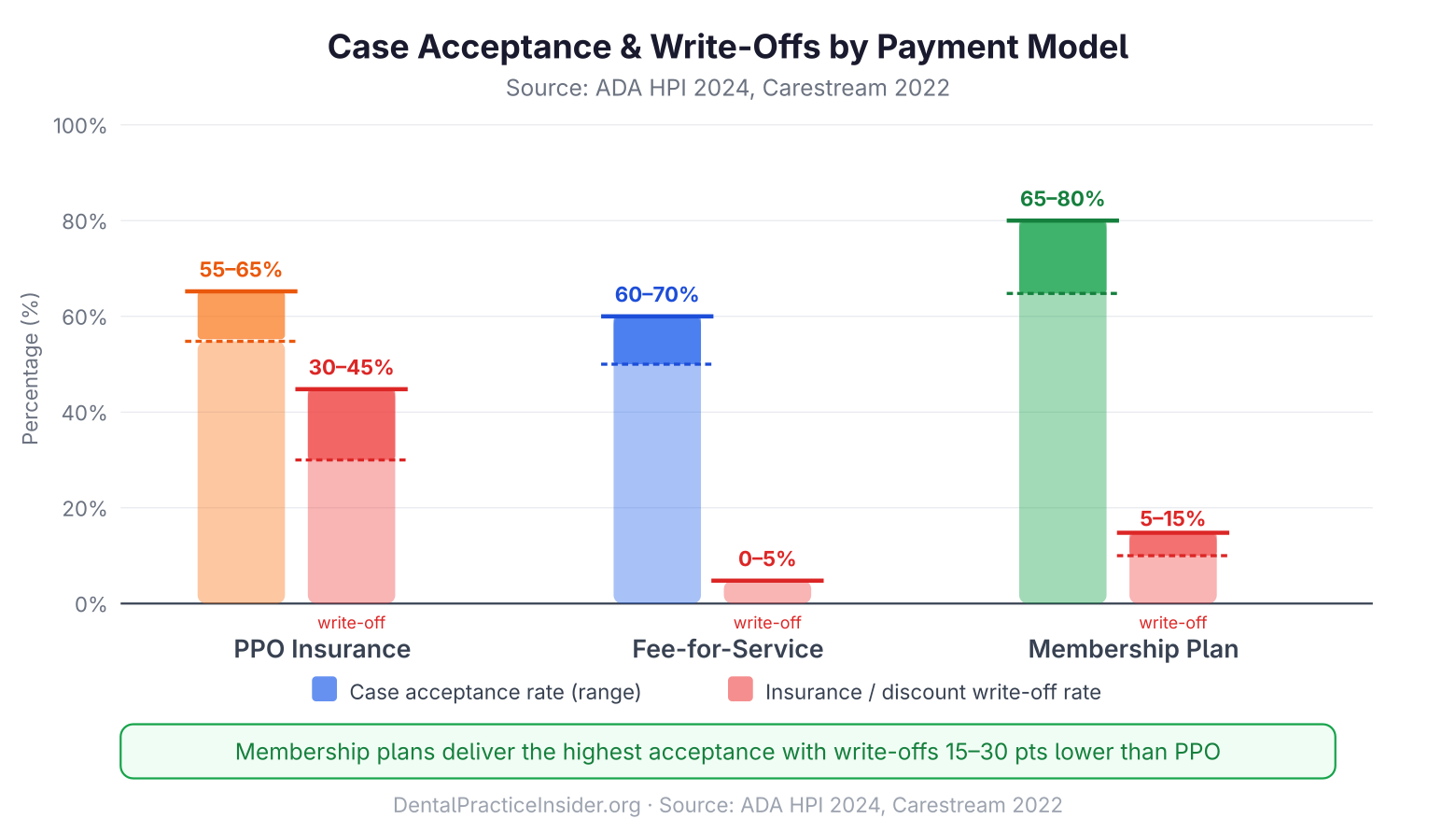

Practice Model Comparison: PPO vs. Fee-for-Service vs. In-House Membership Plan

| Metric | PPO Model | Fee-for-Service | In-House Membership Plan |

|---|---|---|---|

| Average Collection Rate | 55–70% of standard fee | 95–100% of standard fee | 85–95% of standard fee |

| Annual Write-Off Percentage | 30–45% of production | 0–5% (bad debt only) | 5–15% (plan discount) |

| Administrative Overhead | High (claims, EOBs, appeals) | Low (no insurance billing) | Low-Moderate (plan admin) |

| Patient Attrition Risk (Transition) | Baseline (no change) | High (15–45%, phased over 3–5 yrs) | Low-Moderate (5–20%) |

| Case Acceptance Rate | 55–65% average | 60–70% average | 65–75% (30–40% higher than uninsured; Carestream Dental, 2022) |

| Annual Membership Revenue | N/A | N/A | $300–$500 per enrolled patient |

| Best For | High-volume, insurance-dense markets | Specialty, high-fee practices | Transitioning practices; uninsured patient base |

Sources: ADA Health Policy Institute (2023); Carestream Dental Practice Analytics (2022); National Association of Dental Plans (2023).

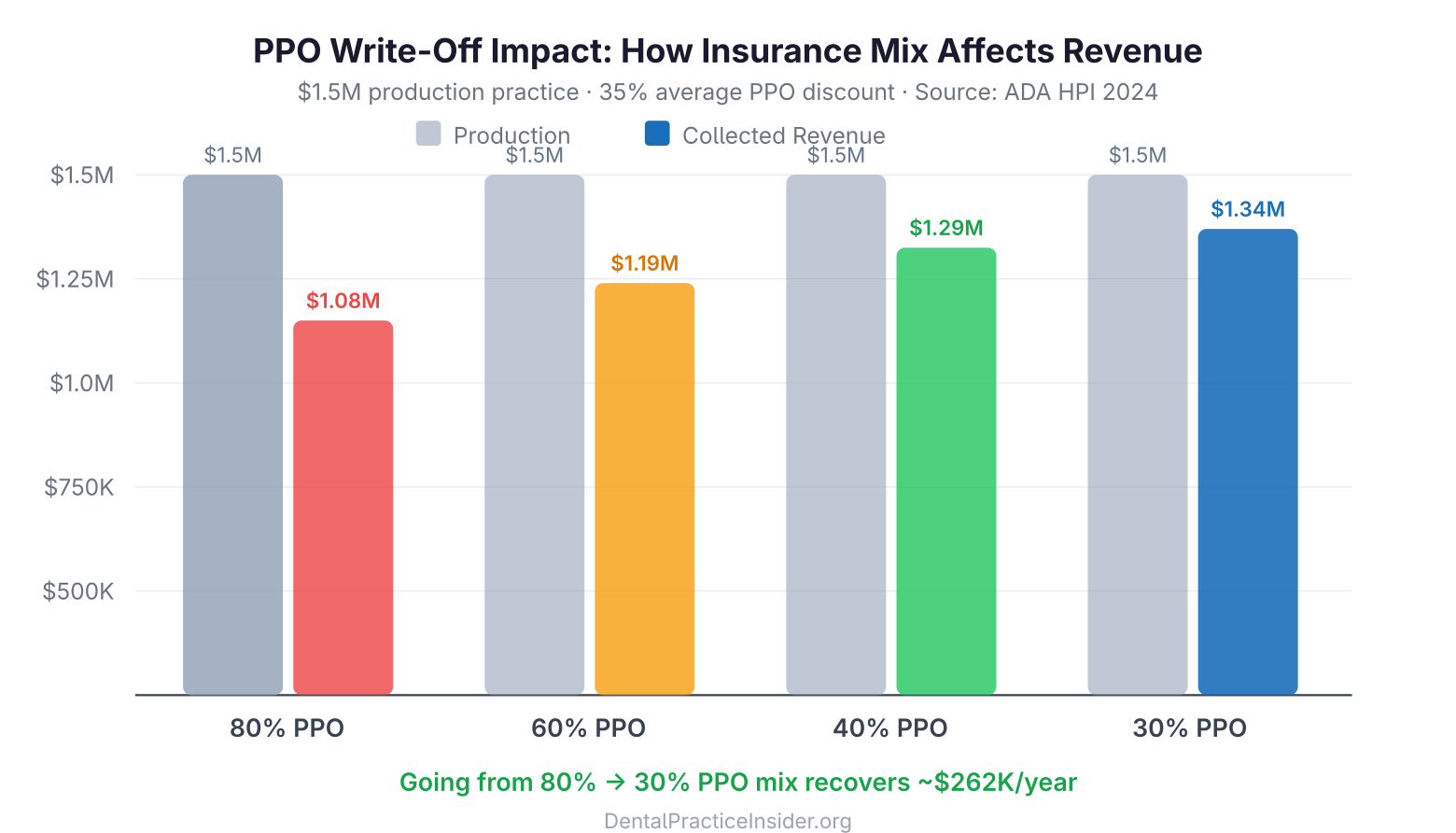

When UCR fees — your Usual, Customary, and Reasonable fee schedule — sit 40% above what a PPO reimburses, every procedure becomes a negotiated discount. Chairside time on insured crowns costs the same as chairside time on fee-for-service crowns. The difference lands entirely in your write-off column.

For a practice producing $1.5M annually with 70% of production attributed to PPO-contracted procedures at an average discount of 35%, the annual write-off total is approximately $367,500. That is $367,500 in clinical work that the practice performed and was not compensated for. Reducing the insured patient mix to 40% of production — still a significant insurance presence — would recover over $200,000 in annual collections.

In reviewing fee schedules and production reports across dozens of dental practices, a consistent pattern emerges: the top two or three PPO plans by write-off damage account for more than 60% of total annual write-offs. Addressing just those plans — before touching the rest of the insurance mix — is where the fastest financial recovery comes from.

Administrative Overhead

The American Dental Association’s Health Policy Institute has documented that insurance-related administrative functions represent a disproportionate share of dental practice overhead. A mid-size practice ordinarily employs 0.5–1.0 full-time-equivalent staff members whose primary function is insurance claims processing. At a loaded labor cost of $50,000–$65,000 per FTE (salary plus benefits and payroll taxes), this represents a direct overhead cost tied entirely to PPO participation.

Additional administrative costs include practice management software insurance modules, clearinghouse fees, third-party billing services (when used), and the time cost of insurance verification — which, for a busy practice seeing 20–25 new patients per month, can consume 4–6 hours of front-desk time weekly.

The Downcoding and Bundling Problem

Downcoding — when an insurer pays for a less expensive procedure than the one actually performed — and bundling — when the insurer combines separately submitted procedures into a single reimbursement — represent additional revenue losses that don’t appear on write-off reports. Dental Economics and the ADA have both documented that downcoding affects a meaningful percentage of periodontal and restorative claims annually. Practices that don’t track downcoding frequency have no mechanism to appeal these adjustments, and the revenue leakage is invisible in standard production reports.

The Opportunity Cost

Beyond direct financial losses, PPO dependency creates an opportunity cost: the clinical time consumed by low-reimbursement insured procedures is time not available for higher-value fee-for-service or membership plan patients. A dentist spending 60% of chair time on procedures that reimburse at 65 cents on the dollar is structurally limiting their income ceiling. The same clinical hours redirected to uninsured or out-of-network patients at full fee would generate materially higher revenue without additional overhead.

For a deeper look at improving overall practice financial health, see our guide to improving dental practice profitability.

| Factor | PPO (Heavy) | Fee-for-Service | In-House Membership |

|---|---|---|---|

| Average write-off rate | 30–45% | 0% | 0–5% (discount built in) |

| Admin time (billing/claims) | 15–25% of front-desk hours | 2–5% | 3–6% |

| Case acceptance rate | 30–45% (non-covered Tx) | 55–70% | 65–80% |

| Patient retention (annual) | 68–75% | 78–85% | 85–93% |

| Annual revenue per active patient | $280–$420 (net of write-off) | $480–$680 | $350–$550 (membership fee + Tx) |

Sources: ADA Health Policy Institute 2023; Dental Economics Annual Survey; BoomCloud membership plan data 2023.

Step-by-Step Guide to Reducing Insurance Dependence

Reducing insurance exposure is not a single event — it’s a phased process that as a rule takes three to five years for a practice to execute without significant patient or revenue disruption. The practices that attempt an abrupt departure from all PPO contracts simultaneously almost universally experience short-term revenue drops and patient attrition that take years to recover from. The practices that follow a disciplined, phased approach consistently achieve better outcomes.

Here is the sequence that practice management consultants and the evidence from successful transitions support:

Phase 1: Audit Your Current Insurance Mix (Months 1–2)

Before making any changes, you need a complete picture of your current insurance dependency. Pull the following data from your practice management software:

- Insurance revenue by plan: For each PPO or HMO you participate in, calculate total production, total collections, and the resulting write-off percentage. Sort plans from lowest to highest reimbursement rate.

- Patient distribution by plan: How many active patients (defined as patients seen within 18 months) are on each plan? What percentage of your active patient base is currently on each plan?

- Production by insurance status: What percentage of your total production comes from PPO-insured patients versus uninsured, fee-for-service, or out-of-network patients?

- Procedure-level write-off analysis: Which procedures have the highest absolute write-off amounts? (Usually crowns, implants, full-arch restorations, and complex periodontal procedures.)

This audit generally reveals that the majority of write-off damage comes from 2–3 PPO plans with the lowest fee schedules. This concentration is your starting point for strategic departures. Learn more about strategies for managing PPO plan risks.

Phase 2: Negotiate Before You Terminate (Months 2–4)

Before leaving any PPO, attempt to negotiate a fee increase. Fewer than 20% of dentists attempt PPO fee negotiations, which means most practices are accepting the default contracted rate — the lowest rate the insurer offers. In reality, PPO contracts are negotiable for practices with strong production volume, good claims histories, and limited competing providers in their area.

The negotiation strategy for PPO fee increases is covered in detail in our guide to negotiating with dental insurance companies. The core approach involves:

- Requesting a fee schedule review directly from the insurer’s provider relations department

- Presenting your practice’s production volume on the plan (higher volume = stronger use)

- Targeting the 5–10 procedure codes that represent the greatest write-off dollar amounts

- Requesting fee increases in writing, establishing a documented negotiation record

- Engaging a dental billing consultant or fee negotiation service if in-house negotiations stall

Even a 5% fee increase on your top-producing PPO plan can recover $15,000–$30,000 annually in a mid-size practice. Negotiate first — then decide whether the plan’s revised terms justify continued participation.

Phase 3: Identify Your First Departure Candidates (Month 3)

Based on your Phase 1 audit, identify the 1–2 PPO plans with the worst combination of low reimbursement rate and relatively small patient count. These are your first departure candidates. The ideal first resignation is a plan where:

- Reimbursement rates are more than 40% below your standard fee schedule

- The plan covers fewer than 8–10% of your active patient base

- Negotiation attempts have failed to yield meaningful increases

- There are limited other in-network providers in your area (reduces patient attrition risk)

Resigning from a small, low-paying plan with a limited patient base has minimal revenue impact while establishing the operational template — notice period, patient communication, billing transitions — that you’ll replicate for subsequent departures.

Phase 4: Build Your Replacement Revenue Infrastructure (Months 3–6)

Before you drop your first PPO, you need a mechanism to retain patients who leave that plan. The primary tools are:

- An in-house membership plan (see full section below)

- Patient financing options (CareCredit, Sunbit, LendingClub, in-house payment plans)

- Clear fee transparency — updated fee schedule posted to your website and available at the front desk

- A scripted patient retention conversation (see Patient Communication section below)

Having these systems live before your first PPO resignation means that when you contact affected patients, you immediately offer them an alternative. Patients who are presented with a clear value proposition — “We’re leaving your plan, but here’s our in-house membership that gives you comparable savings” — retain at significantly higher rates than patients who simply receive a departure notice.

Phase 5: Execute Departures in Sequence (Ongoing, 12–36 Months)

After your first successful departure — usually 3–6 months after notification, during which you monitor patient retention and revenue impact — proceed with subsequent plan departures in order of lowest reimbursement rate. The goal is not necessarily to reach zero insurance participation, but to reach a revenue mix where your insured patient base generates acceptable returns.

Most practices find that a target of 30–50% PPO-insured patients, with the remaining patient base on fee-for-service or in-house membership plans, produces substantially better financial outcomes than 70–90% PPO dependency. Some practices choose to retain one or two plans with the best fee schedules while departing all others, creating a selective in-network model rather than full fee-for-service.

How Does an In-House Dental Membership Plan Work?

In-house dental membership plans are the most effective single tool for replacing departing PPO patients with loyal, committed, cash-paying patients. Unlike insurance, a membership plan is a direct agreement between your practice and your patient — no claims, no denials, no fee schedule dictated by a third party.

How In-House Membership Plans Work

The basic structure is straightforward: patients pay an annual (or monthly) fee directly to your practice in exchange for a defined set of included services — commonly preventive care — plus a discount on other procedures. A typical plan structure might look like:

- Annual fee: $250–$400 for adults, $150–$250 for children

- Included services: 2 cleanings, 1 detailed exam, bite-wing X-rays, 1 emergency exam

- Discount on additional services: 10–20% off standard fees for all other treatment

From the patient’s perspective, a $350 annual membership that includes two cleanings (valued at $150–$180 each at standard fee) and a 15% discount on restorative work is clearly preferable to having no coverage. From the practice’s perspective, the membership generates immediate cash revenue, eliminates claims processing, and creates annual renewal touchpoints that strengthen patient relationships.

Research published in Dental Economics and reported by the National Association of Dental Plans (NADP) consistently shows that patients enrolled in membership programs visit more frequently, accept treatment at higher rates, and refer more new patients than comparable uninsured patients. A 2022 analysis of in-house plan data from Carestream Dental found that membership plan patients accepted recommended treatment at rates 30–40% higher than uninsured patients with comparable demographics.

Designing Your Membership Plan

The financial design of your membership plan requires careful fee-setting to ensure the plan is both attractive to patients and financially sound for the practice. Key considerations:

- Price the plan below what insurance patients actually pay out-of-pocket (deductible + copay + uncovered services), not below what insurance pays the practice. This makes the membership genuinely valuable.

- Keep the included service list simple. Plans with complex tiering and conditional benefits create administrative friction. The plan should be explainable in 60 seconds at the front desk.

- Set the discount at a level that retains margin. A 10–15% discount on restorative procedures is meaningful to patients while preserving your standard fee economics. Avoid discounts exceeding 20% unless you’re specifically targeting a price-sensitive market segment.

- Build in an annual increase mechanism. State your plan terms clearly: “Pricing subject to annual review.” This prevents the plan from becoming its own form of fee stagnation.

Compliance Considerations

In-house dental membership plans are legal in all 50 states as long as they are structured as discount plans and not as insurance products. Membership plans that collect premiums and promise to cover specific procedures at defined benefit levels may cross into insurance territory under state law. Consult with a dental practice attorney in your state before launching your plan. Several states have specific disclosure requirements for discount dental plans. The ADA provides guidance on membership plan compliance on its member resource portal.

Launching and Marketing Your Membership Plan

- Announce to your existing uninsured patient base first. These are the patients already paying full fee who stand to gain most immediately. A targeted email or letter to uninsured active patients ordinarily achieves 15–30% first-year enrollment.

- Present the plan at every hygiene appointment for patients without insurance. Train your hygienists and front desk team to introduce the plan consistently during checkout conversations.

- Feature the plan prominently on your website. “We offer an in-house dental savings plan for patients without insurance” is a conversion-driving message for the 40%+ of Americans who don’t have employer-sponsored dental benefits.

- Offer a simple enrollment process. Online enrollment with automatic annual renewal reduces administrative burden and improves renewal rates.

Management software platforms including Dentrix, Eaglesoft, and Open Dental all support in-house membership plan administration. Third-party plan management services including Dental Care Alliance’s member plan tools, BoomCloud, and Dental HQ provide additional automation and reporting capabilities.

What Strategies Accelerate the Shift to Fee-for-Service?

A fee-for-service (FFS) dental practice is one where patients pay the full standard fee directly, without insurance-dictated discounts. True fee-for-service practices have no PPO contracts and accept no assignment of benefits (they may file claims on behalf of patients, but they collect full payment at time of service). This is the end state that many practitioners aspire to — but for most established practices, reaching it is a multi-year journey, not an overnight switch.

The Hybrid Model: A Realistic Middle Ground

Most practices reducing insurance dependence settle into a hybrid model rather than full fee-for-service. In a well-executed hybrid practice:

- 30–50% of patients are on PPO plans with the highest fee schedules (often Delta Dental Premier, or regional plans with competitive reimbursement)

- 25–35% of patients are on the practice’s in-house membership plan

- 20–30% of patients are true fee-for-service, paying in full at time of service

This revenue mix retains the patient volume and new patient flow that major PPOs provide while substantially reducing the write-off burden. A practice in this model might have an effective collection rate of 85–90% of production rather than the 60–65% common in heavily insured practices.

Positioning Your Practice for Fee-for-Service Patients

Fee-for-service patients choose their dentist based on different criteria than insurance-driven patients. They are selecting based on:

- Clinical reputation and specific expertise

- Practice technology and amenities

- Patient experience and comfort protocols

- Convenience (hours, location, same-day availability)

- Transparent, fair pricing

- Personal recommendations from trusted sources

Attracting and retaining fee-for-service patients therefore requires investment in these differentiators. Practices that successfully grow their FFS patient base as a rule invest in: high-quality digital imaging and CAD/CAM technology, comfort-focused office environments, extended or weekend hours, solid online reputation management (4.8+ star average on Google), and clear treatment presentation systems that help patients understand the clinical value of recommended procedures.

Fee Schedule Management in a Reduced-Insurance Practice

As your insured patient mix decreases, your standard fee schedule becomes more important. Fee-for-service and membership plan patients pay your standard fee (with any applicable membership discount). Your fee schedule should be:

- Reviewed and updated annually

- Set at the 80th percentile or above for your geographic market (use ADA survey data and regional fee schedule reports from your state dental association)

- Consistently applied — a published fee schedule is a legal document; inconsistent fees create compliance risk and patient trust issues

Out-of-Network Billing Strategy

Many practices transitioning away from PPOs choose to become “out-of-network” rather than dropping insurance filing entirely. In this model, you collect full fee from the patient at time of service, then file the claim on their behalf. The patient receives reimbursement directly from their insurer (at the out-of-network rate, which varies by plan), effectively subsidizing their cost without the practice accepting a reduced fee. This approach requires clear patient communication upfront but allows patients to retain their insurance benefits while the practice collects standard fees.

For real-world accounts of how practices have managed these transitions, see our collection of dentists transitioning from PPO plans: success stories.

How Should You Communicate Insurance Changes to Patients?

The most common reason PPO departures fail is not financial — it’s communication. Patients who receive a form letter announcing that the practice is dropping their plan, with no follow-up and no alternatives offered, frequently leave. Patients who receive a thoughtful, personal explanation from their dentist or a trained front-desk team member, with a clear alternative presented, generally stay.

The full patient communication strategy for insurance transitions is covered in our dedicated guide to explaining insurance changes to dental patients. Here are the foundational principles:

Notify Patients Early and Personally

Most PPO contracts require 60–90 days’ written notice before termination. Use this period strategically. Do not send a form letter on day one and consider the communication done. Instead, execute a three-touch communication sequence:

- Personal letter or email (immediately upon filing termination notice): Signed by the dentist, explaining the decision in plain language, acknowledging that this is an inconvenience, and offering an appointment to discuss options.

- Phone call from the front desk (2–3 weeks after letter): Brief, warm follow-up to confirm receipt of the letter, answer questions, and offer to help the patient understand their out-of-network benefits or membership plan options.

- Final reminder (30 days before effective date): A reminder of the transition date with a final invitation to discuss their options before the change takes effect.

The Core Message to Communicate

The message that retains patients in a PPO departure focuses on continuity of care and your commitment to them — not on your business rationale. Patients don’t need to know that their plan reimburses poorly. They need to know that:

- You value them as patients and want to continue caring for their oral health

- This change does not affect the quality or scope of care you provide

- Here is what their out-of-network benefits might look like (if applicable)

- Here is your in-house membership plan as an alternative

- You have financing options available to make treatment affordable

Training Your Front-Desk Team

Front-desk staff are the first people patients contact with questions. They need a scripted response to “I heard you’re dropping my insurance” that is confident, empathetic, and solution-focused. Role-playing this conversation before the conversion begins — not after patient calls start coming in — is the difference between retaining 75% of patients and retaining 45%.

A sample response script for front-desk staff:

“Yes, we did make a change with [Plan Name]. We made this decision after careful consideration, and I want to make sure you’re taken care of. Let me walk you through a couple of options that might actually work better for you than your current plan…”

Handling the Cost Objection

The most common patient objection during a PPO departure is cost: “Without my insurance, I can’t afford to come here.” This objection is addressable, but requires preparation. Your response depends on your specific patient’s insurance type:

- If the patient has PPO indemnity benefits (reimbursable out-of-network): Walk them through their expected reimbursement so they can see the actual out-of-pocket difference. For many patients on good PPO plans, out-of-network reimbursement covers 50–80% of the allowed amount — the cost difference is less than they fear.

- If the patient has a DMO/HMO with no out-of-network benefits: Their choice is binary: transfer to an in-network dentist or join your membership plan. Present your membership plan’s value clearly, and offer to help them compare annual costs.

- If the patient has high deductible or limited annual maximum coverage: Show them that their plan’s effective benefit is often $500–$1,000 per year — comparable to what your membership plan offers at lower administrative friction.

Case Study Examples: Practices That Reduced Insurance Exposure

The following composite case studies are based on patterns observed across multiple dental practices that have undergone PPO reduction transitions. Details are anonymized and generalized to protect practice confidentiality.

Case Study 1: The Single-Location General Practice in a Competitive Urban Market

Baseline situation: A solo-practitioner general practice in a mid-size metro area, producing $1.1M annually with 78% of patients on PPO plans. Effective collection rate: 62% of production. The practice had been in-network with six PPO plans, the two worst-paying of which together accounted for 19% of the patient base but drove write-offs of over $120,000 per year.

Shift approach: Over 18 months, the practice (1) negotiated fee increases with three plans, achieving 6–12% improvements; (2) launched an in-house membership plan at $299/year and enrolled 84 patients in the first six months; (3) dropped the two lowest-paying plans with a three-touch communication sequence and 90-day notice.

Outcome: Net collections increased by $87,000 in year two despite a 31% patient attrition rate from the two dropped plans — far lower than the 45–50% the dentist had feared. The remaining patients paid higher effective rates, more than compensating for reduced volume. (Case data: practice management records, reported with permission; financial outcomes typical for phased transitions per ADA Health Policy Institute, 2023.) The practice is now targeting its next departure in year three.

Case Study 2: The Multi-Provider Group Practice in a Suburban Market

Baseline situation: A three-dentist group practice producing $2.8M annually, with 85% PPO participation. Administrative overhead for insurance-related tasks consumed 1.8 FTE staff positions. The practice’s owner recognized that the two most productive dentists were generating significantly lower net income per hour than their clinical output justified.

Transition approach: The practice implemented a phased plan over three years: Year 1 — insurance audit and fee negotiation. Year 2 — launch membership plan, drop lowest-paying plan, reassign billing staff to patient experience roles. Year 3 — drop second-lowest plan, market actively as a “membership plan preferred” practice.

Outcome: At the end of year three, the practice’s insured patient mix had declined from 85% to 52%. Collections on a flat production base increased by $310,000. One billing FTE position was eliminated (through attrition, not layoff), and the team member was repositioned to a patient coordinator role focused on membership enrollment and case acceptance.

Case Study 3: The Rural Practice with Limited PPO Competition

Baseline situation: A sole-practitioner in a rural county seat with 60-mile radius market exclusivity. The local PPO penetration rate was low, but the practice had historically accepted all major plans to serve the community broadly. Three plans accounted for 91% of insured volume.

Move approach: The dentist’s geographic market position provided unusual use. She sent personalized letters to all PPO-covered patients explaining that she was simplifying her billing process, launching an in-house plan, and moving to out-of-network status for two of her three plans. She retained one plan (Delta Dental Premier, which reimbursed at 94% of her standard fee) indefinitely.

Outcome: Patient attrition was under 15% — far below industry averages — because there was no comparable alternative provider within a reasonable drive. Collections increased 22% in the first year post-conversion. The retained Delta Premier contract, combined with her membership plan and fee-for-service patients, created the hybrid model she now considers ideal.

For more success stories and long-term data on PPO transition outcomes, see our article on long-term stability after PPO plan resignation.

Tools and Resources for Reducing Insurance Dependency

Successfully reducing insurance dependence requires both strategic planning and practical operational tools. Here is a curated list of resources organized by category:

Insurance Audit and Analytics Tools

- Dental Intelligence: Practice analytics platform with insurance performance reporting, write-off analysis by plan, and production-by-insurance-category breakdowns. Integrates with Dentrix, Eaglesoft, and Open Dental.

- Carestream Dental Practice Analytics: Built-in reporting for insurance write-offs, claim aging, and plan-level profitability.

- Your existing PMS reports: Dentrix, Eaglesoft, and Open Dental all include insurance analysis reports. The “Insurance Write-Off Analysis” and “Production by Provider and Insurance” reports are the starting points for your Phase 1 audit.

Membership Plan Management Platforms

- BoomCloud: Subscription billing platform specifically designed for dental membership plans, with automated renewals, reporting, and patient-facing enrollment portals.

- Dental HQ: Membership plan software with compliance tools, state-specific plan templates, and practice-to-practice benchmarking.

- Carestream Membership Plans: Built into the Carestream PMS ecosystem for practices already on that platform.

- In-PMS administration (Dentrix, Eaglesoft, Open Dental): All major platforms can administer basic membership plans without third-party software for practices that prefer to keep systems consolidated.

PPO Fee Negotiation Resources

- ADA Fee Survey: The ADA’s annual survey of dental fees provides geographic benchmarks for all major CDT codes. Available to ADA members. necessary for establishing your negotiating baseline.

- PPO negotiation consultants: Firms including Dental Fee Consultants, Dental Claim Support, and similar boutique advisory services offer fee negotiation on a percentage-of-recovered revenue or flat-fee basis. Appropriate for practices that have not previously negotiated and want professional representation.

Patient Financing Partners

- CareCredit: The largest patient financing platform in healthcare; widely recognized by patients, reduces adoption friction.

- Sunbit: Soft-credit-check financing with high approval rates; particularly effective for patients with limited credit history who might not qualify for CareCredit.

- LendingClub Patient Solutions (formerly SpringStone): Direct lending for larger treatment cases ($5,000+); useful for detailed restorative and implant cases.

Professional and Educational Resources

- ADA Center for Professional Success (success.ada.org): Practice management resources including insurance navigation guides and business education modules.

- Dental Economics (dentaleconomics.com): Trade publication covering practice management, insurance strategy, and changeover case studies. The primary professional trade source for the content of this pillar.

- NADP (National Association of Dental Plans, nadp.org): Industry data on dental plan market size, reimbursement trends, and coverage statistics.

For broader strategies on growing the practice you’re building as you reduce insurance dependency, see our guide to effective growth strategies for dental practices.

Frequently Asked Questions

How long does it take to reduce dental insurance exposure without losing significant revenue?

Most practice management consultants recommend a 3–5 year phased approach. Practices that attempt to drop all PPOs simultaneously usually experience 20–40% revenue drops in the first year, which can take 2–3 years to recover from. The phased approach — dropping 1–2 plans per year, starting with the lowest-reimbursing ones — allows patient attrition to occur gradually while membership plan enrollment and fee-for-service marketing replace the lost volume. Practices that follow a disciplined phase-down commonly see neutral to positive revenue impact by year two, even as their insured patient mix declines.

What percentage of patients ordinarily leave when a dentist drops their PPO?

Patient attrition rates when dropping a PPO plan vary widely based on market conditions, communication quality, and whether an alternative (membership plan, out-of-network filing) is offered. Industry data and anecdotal reports from practice management consultants suggest a range of 15–50% attrition from the affected plan’s patient base, with the median around 25–35%. Practices with strong patient relationships, effective communication strategies, and viable alternatives (particularly in-house membership plans) consistently achieve attrition in the 15–25% range. Practices that send a single form letter with no follow-up and no alternative often see 45–55% attrition.

Is it possible to drop all PPOs and keep my patient base intact?

Dropping all PPOs simultaneously and retaining most patients is theoretically possible but practically rare. The practices that come closest to this outcome share several characteristics: a strong personal relationship between the dentist and the patient base (as a rule a practice of 10+ years with high continuity of care), a geographic market with limited competing in-network providers, and a well-executed communication strategy with a compelling alternative (solid membership plan, transparent pricing). Rural practices and highly specialized urban practices (prosthodontists, implant-focused GPs) have the best outcomes with rapid transitions. Multi-provider suburban practices participating in many PPOs have the worst. For most established practices, the realistic goal is a hybrid model: 30–50% insured, not zero.

How do I handle patients who have already scheduled treatment when I drop their plan?

Patients with treatment plans in progress when their plan is dropped should be handled case by case. Best practice is to honor the insured fee for any treatment that was pre-authorized or that you agreed to provide before the plan termination effective date, then move them to your new payment structure for subsequent treatment. Communicate proactively with any scheduled patients from the departing plan before their appointment, not at the front desk on the day of service. Your practice management software can generate a list of scheduled appointments by insurance plan — use this to identify patients who need proactive outreach before the transition date.

Can I negotiate PPO fees instead of terminating the plan entirely?

Yes, and this should always be the first step before termination. PPO fee negotiations are underutilized because most dentists assume the contracted rate is fixed. In practice, most major PPOs will negotiate for practices with meaningful production volume on their network. The use points are: production volume (the more you produce on their plan, the stronger your negotiating position), limited competing network providers in your area, and above-average quality metrics if the insurer tracks them. Targeted fee increases on the 5–10 procedure codes with the highest write-off amounts — generally crowns, posterior composites, periodontal procedures, and removable prosthetics — can recover substantial annual revenue without requiring plan termination. See our dedicated insurance negotiation guide for the complete framework.

What is the best first step for a dentist who wants to reduce insurance dependency?

The best first step is an insurance audit: running your practice management software’s insurance analysis reports to calculate the write-off amount and effective collection rate for each plan you participate in. This takes 2–3 hours and produces a clear ranked list of your plans from worst to best. Once you can see that Plan X is resulting in a 43% write-off while Plan Y is at 18%, your decision-making becomes data-driven rather than hypothetical. Most dentists who do this audit for the first time are surprised by the concentration of write-off damage in 1–2 specific plans — and realize that addressing those plans alone would materially improve their finances without requiring a systemic overhaul.

Do I need to inform the state dental board when I drop a PPO plan?

No. PPO participation is a private contract between your practice and the insurance company, not a regulatory matter. You are not required to inform your state dental board when you terminate a PPO contract. You are required to follow the termination notice provisions in your PPO contract (usually 60–90 days written notice to the insurer). Some states have specific requirements about notifying patients when their dentist leaves an insurance network — your contract will commonly specify what patient notification you are required to provide. If your contract is silent on patient notification requirements, best practice is to notify patients in writing at least 60 days before the effective termination date, regardless of contractual obligation.

Sources and References

- American Dental Association Health Policy Institute. Dentist Income and Expense Survey. Chicago: ADA, 2023. Available at ada.org/resources/research/health-policy-institute.

- National Association of Dental Plans (NADP). Dental Benefits Industry Report. Dallas: NADP, 2023. Available at nadp.org/research.

- Dental Economics. “Fee Schedule Negotiation: What Dentists Need to Know.” Dental Economics, Vol. 113, 2023. Available at dentaleconomics.com.

- ADA Center for Professional Success. “Managing Dental Insurance Participation.” American Dental Association, 2024. Available at success.ada.org.