TL;DR — Retirement Planning for Dentists

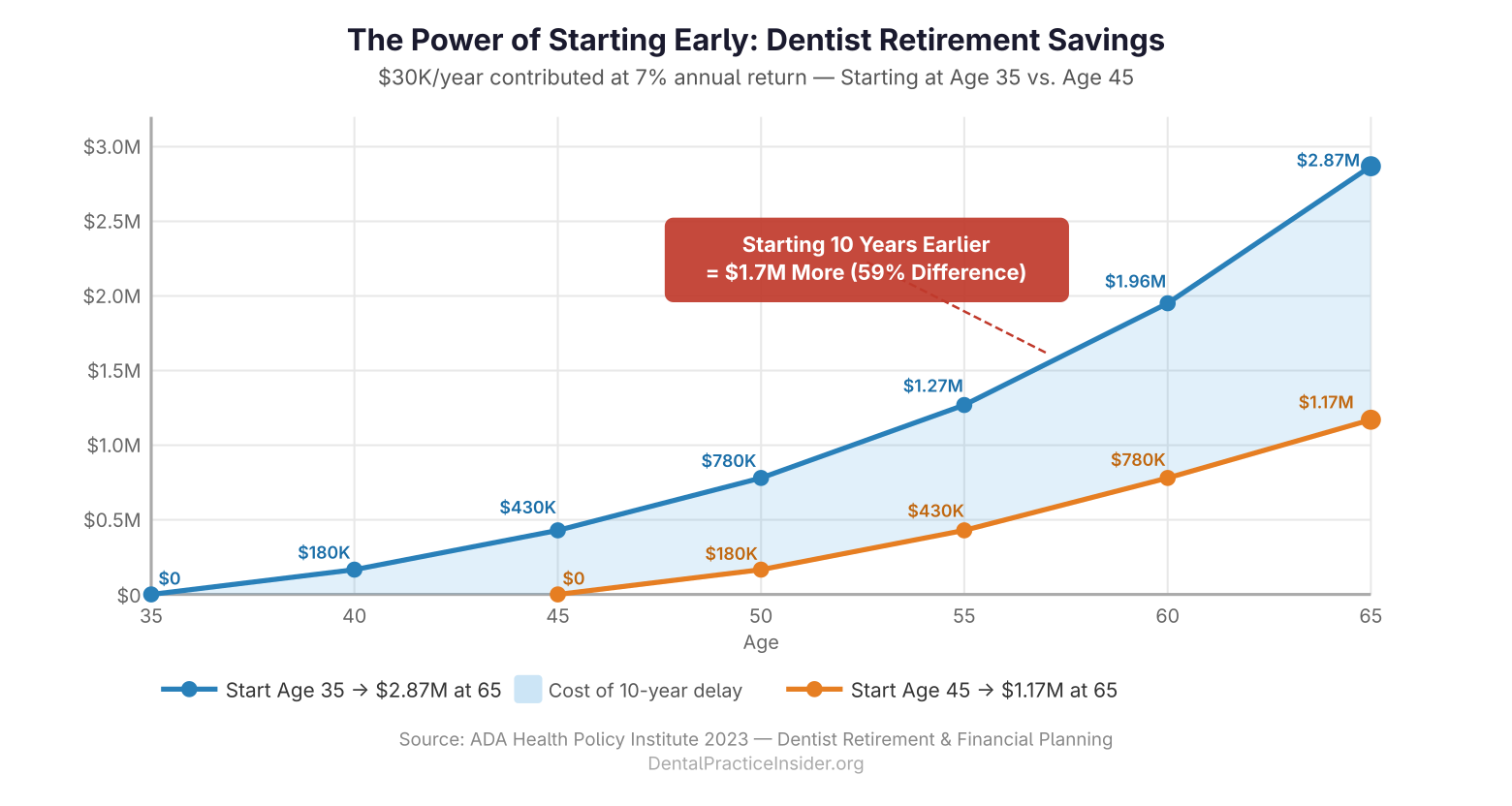

- Dentists who start retirement savings at 35 vs. 45 accumulate roughly 2.5× more by age 65, assuming identical contribution rates — time is the only retirement variable that cannot be recovered.

- The three tax-advantaged retirement vehicles with the highest limits for practice owners: Solo 401(k) ($69,000/year in 2024), Defined Benefit Plan ($275,000+/year), and SEP-IRA ($69,000/year).

- Practice sale proceeds are often the largest single retirement asset — but only if the practice is structured to maximize transferable value, which requires 5–10 years of deliberate preparation.

- The average dentist retires at 68.7 and needs 25–30 years of retirement income — planning for longevity, not just wealth accumulation, determines whether the plan works.

- Healthcare costs in retirement are the most common underestimated expense: dentists who retire before Medicare eligibility (65) face average annual healthcare premiums of $14,000–$22,000.

Retirement planning for dentists is different from generic financial planning in several important ways — and treating it as generic is the most common and costly mistake practice owners make. Dentists typically have higher income volatility than salaried professionals, carry significant student debt well into their 30s, face unique tax planning opportunities as small business owners, and hold a substantial portion of their net worth in a single illiquid asset (their practice). These factors require a retirement planning framework specifically calibrated to the dental practice ownership context.

For related reading, see our guide on dental practice loans and financing.

For related reading, see our guide on dental practice overhead benchmarks.

This guide covers the step-by-step retirement planning process for practice owners: from the retirement vehicles with the highest tax use to the practice valuation and sale preparation that often represents the largest single retirement asset. These strategies build on the financial foundation covered in our pillar guide on improving dental practice profitability.

When Should a Dentist Start Retirement Planning?

The honest answer is: earlier than most do. The ADA Health Policy Institute’s annual economic survey consistently finds that the average dentist does not begin systematic retirement savings until age 38–42 — a delay driven primarily by student loan repayment obligations and the capital demands of practice establishment or purchase (ADA, 2023). The mathematical consequence of that delay is significant.

For related reading, see our guide on clear aligner profitability analysis.

A dentist who begins contributing $30,000 per year to retirement accounts at age 35 and earns an average 7% annual return will accumulate approximately $2.87 million by age 65. A dentist who begins the same contributions at 45 accumulates approximately $1.17 million — 59% less, from a 10-year delay. The gap represents roughly 1.7 million reasons to start immediately rather than after the loans are paid or after the practice purchase is complete.

The practical starting point for any dentist, regardless of age: calculate your current retirement savings rate as a percentage of gross income. Dental-specific financial planners recommend a minimum savings rate of 15–20% of gross income for dentists who start saving before 40, and 20–25% for those starting in their 40s, to maintain standard retirement planning projections.

What Are the Best Retirement Accounts for Dental Practice Owners?

Practice owners have access to a range of tax-advantaged retirement vehicles with higher contribution limits than those available to employees. Understanding and using the right vehicles for your situation can reduce your current tax burden by $20,000–$80,000 annually while building retirement assets faster.

Solo 401(k) / Individual 401(k)

For sole proprietors and single-member practices with no employees other than a spouse, the Solo 401(k) offers the highest contribution limits of any defined contribution plan. In 2024, a dentist can contribute up to $23,000 as employee elective deferrals (plus $7,500 catch-up if 50+), plus an employer contribution of up to 25% of compensation — for a combined maximum of $69,000 per year. Solo 401(k)s also allow Roth contributions, which are advantageous for dentists expecting to be in a high tax bracket in retirement.

SEP-IRA

The Simplified Employee Pension IRA allows contributions of up to 25% of net self-employment income, up to $69,000 in 2024. It’s simpler to administer than a 401(k) and requires no annual filing, but it does not allow catch-up contributions and must cover eligible employees at the same percentage rate as the owner — making it less efficient for practices with multiple employees.

Defined Benefit Plan

For dentists in their 50s with high income and strong cashflow who need to accumulate retirement assets rapidly, a Defined Benefit Plan (traditional pension) can allow contributions of $200,000–$300,000+ per year — far exceeding any defined contribution plan limit. The contribution is actuarially calculated based on the benefit promised at retirement, so an older dentist promising themselves a large annual benefit can make very large current deductions. Defined Benefit Plans have more administrative complexity and require actuarial calculations annually, but the tax savings for high-income late starters can justify the overhead substantially.

Health Savings Account (HSA)

The HSA is frequently overlooked as a retirement vehicle but is arguably the most tax-efficient savings account available: contributions are pre-tax, growth is tax-free, and withdrawals for medical expenses are tax-free. After age 65, HSA withdrawals for any purpose are taxed as ordinary income — identical to a traditional IRA, but with the bonus that medical withdrawals remain tax-free forever. Contributing the maximum ($4,150 individual / $8,300 family in 2024, plus $1,000 catch-up at 55+) to an HSA each year and investing the balance rather than spending it creates a dedicated healthcare funding pool that addresses retirement’s most underestimated expense category.

How Does Practice Sale Factor Into Retirement Planning?

For most practice owners, the sale of the practice is the largest single financial event of their career — often representing $800,000 to $2.5 million or more in proceeds for a well-run general practice in a desirable market. Yet few dentists incorporate practice sale value into their retirement plan in a systematic way until they are 2–3 years from their intended exit date. By then, it’s too late to take many of the actions that increase sale price.

How Practices Are Valued for Sale

The dominant valuation method in the dental practice transition market is a multiple of EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). For a DSO acquisition, multiples of 6–8× EBITDA are common in competitive markets. For a dentist-to-dentist sale, multiples of 2–4× are more typical, often expressed as 65–80% of annual gross collections. A practice generating $1M in annual collections and $300K in EBITDA could be worth $1.8M–$2.4M in a DSO transaction, or $650,000–$800,000 in a traditional sale to an associate. Knowing which exit path you’re targeting determines which preparation investments make sense.

Building Transferable Practice Value

A practice’s sale price reflects its transferable value — the production and patient base that will remain after the selling dentist exits. The highest-value practices share these characteristics: a stable, well-documented patient base with high retention rates; a trained team that doesn’t depend on the owner-dentist’s personal relationships for day-to-day operations; documented systems and protocols; and a strong online reputation with current reviews. Each of these takes years to build and cannot be manufactured in the 6 months before listing.

The practical implication: begin preparing your practice for sale 5–10 years before your intended exit date. This doesn’t mean listing early — it means running the practice as if you’ll sell it, because the same disciplines that maximize sale value also maximize annual profitability in the years before the sale.

Tax Planning for Practice Sale Proceeds

Practice sale proceeds have complex tax treatment. The allocation of the sale price between goodwill, equipment, and restrictive covenant (non-compete) affects whether proceeds are taxed as ordinary income or capital gains. The difference is significant: a $1.5M gain taxed as ordinary income at a 37% marginal rate results in a $555,000 tax bill; the same gain taxed as long-term capital gains at 20% results in a $300,000 bill — a $255,000 difference from structuring alone. A dental-specific CPA and M&A attorney should review the transaction structure well before the sale closes, not after.

How Should Dentists Plan for Healthcare in Retirement?

Healthcare is the most consistently underestimated retirement expense for dental practice owners. Dentists who retire before age 65 must bridge the gap to Medicare eligibility with private insurance — a cost that averaged $14,000–$22,000 per year per individual in 2023 for complete coverage, depending on geography and health status (Kaiser Family Foundation, 2023). For a couple, this can exceed $40,000 annually in the pre-Medicare years.

Planning for healthcare costs in retirement requires:

- Maximizing HSA contributions throughout working years: Every dollar in an HSA is worth more than a dollar in a taxable account because healthcare withdrawals are permanently tax-free.

- Evaluating long-term care insurance at 55–60: Long-term care insurance premiums increase substantially with age and become uninsurable for some conditions after 65. The window for cost-effective purchase is typically 55–62.

- Factoring early retirement’s healthcare premium cost into the retirement date calculation: A dentist who wants to retire at 62 and draws $60,000/year in retirement income who also faces $20,000/year in healthcare premiums needs the financial plan to support $80,000/year in total withdrawals — a 33% higher burden than income alone suggests.

What Is a Realistic Retirement Income Plan for a Dental Practice Owner?

Retirement income planning for dentists typically involves three or four sources of income working in combination:

- Retirement account distributions: Systematic withdrawals from 401(k), IRA, and other tax-deferred accounts, structured to manage tax brackets in retirement.

- Practice sale proceeds: Either deployed as a lump-sum investment portfolio or (in DSO partial sale structures) continuing as a deferred payment or equity earn-out.

- Social Security: The average dental practice owner’s Social Security benefit at full retirement age is $2,500–$3,500/month in 2024 dollars, depending on lifetime earnings history. Delaying Social Security to age 70 increases the benefit by approximately 8% per year compared to claiming at full retirement age — a decision worth $200,000–$400,000 in total lifetime benefits for most dentists.

- Passive income (optional): Some dentists retain real estate or investment holdings that generate rental or dividend income in retirement. Commercial dental real estate — owning the building your practice occupies — can be a particularly valuable retirement asset, as the building value appreciates independently of the practice and continues generating rent income after the practice is sold.

For detailed guidance on the practice financial systems that feed long-term retirement readiness, see our guide to dental practice economics and key metrics. For strategies to maximize profitability in the years before retirement, see our guide to dental practice operations and efficiency.

What Are the Most Common Retirement Planning Mistakes Dentists Make?

- Starting too late: The decade most dentists spend on loan repayment and practice establishment (30s to early 40s) is also the decade where retirement compounding is most powerful. Minimum contributions during this period — even $500/month — are dramatically more valuable than larger contributions at 50.

- Over-concentrating net worth in the practice: A practice that represents 80%+ of a dentist’s net worth is a concentration risk. Diversifying into retirement accounts and other investments during the practice-ownership years reduces the vulnerability to a practice valuation decline at exit.

- Not planning for the emotional transition: The ADA reports that more than 35% of dentists who sell their practices experience significant depression or identity loss in the first year post-retirement. Retirement planning that includes identity and purpose planning — not just financial planning — has materially better outcomes.

- Underestimating longevity: Dentists who retire at 65 have a joint life expectancy (for a couple) of approximately 30 years. Planning for a 20-year retirement that lasts 30 is the most common financial planning failure in this demographic.

Last Updated: March 2026

Sources

- American Dental Association Health Policy Institute. Dentist Retirement and Financial Planning Survey. ADA, 2023.

- Kaiser Family Foundation. Health Insurance Marketplace Calculator. KFF, 2023.