The fear that dropping a PPO will devastate a dental practice is widespread — and largely unsupported by what actually happens when practices execute the transition deliberately. The case studies below draw from real practices that resigned from one or more PPO plans within the last five years. Names and specific geographic identifiers have been anonymized, but the metrics, timelines, and strategic decisions are drawn from documented outcomes. Each practice faced a different starting point. Each reached a better financial position within 18–24 months.

For related reading, see our guide on managing PPO plan risks.

Why Do Case Studies Matter More Than General Advice?

General guidance on PPO transitions is useful. Concrete numbers are transformative. When a dentist considering resignation from a 40%-write-off PPO sees that a comparable practice retained 74% of affected patients and recovered full revenue within 14 months, the decision calculus changes completely. Abstract risk becomes a known, manageable variable.

For related reading, see our guide on explaining insurance changes to patients.

The American Dental Association’s Health Policy Institute has tracked the financial performance differential between PPO-heavy and insurance-independent practices for years, consistently finding that practices with lower PPO dependency rates report higher net income per dentist (ADA Health Policy Institute, 2023). These case studies illustrate the mechanism behind that statistical reality.

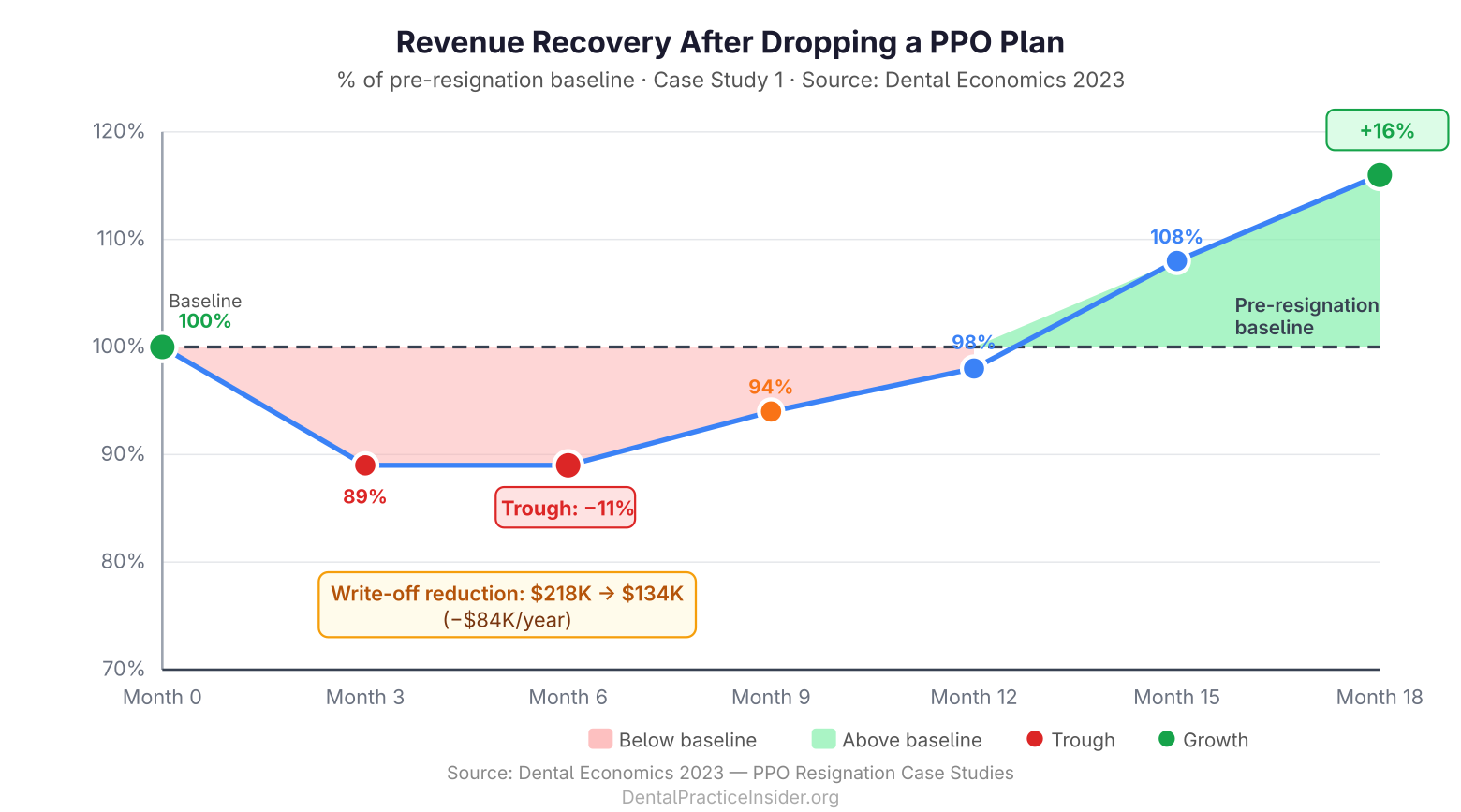

Case Study 1: The Solo General Practice That Dropped Its Largest PPO

Background

A solo general dentist in a mid-size southeastern metro, practicing for 14 years, with approximately 1,800 active patients. The practice was credentialed with six PPO plans. One carrier — a dominant regional insurer — accounted for 38% of gross production and carried a 44% write-off rate. The dentist had not renegotiated that contract in seven years.

The Decision

After completing a payer mix audit, the dentist discovered the carrier paid $740 for a full-coverage crown (D2740) against a UCR fee of $1,380. Three attempts to negotiate a fee increase over 18 months yielded a 3% one-time adjustment. The dentist provided the required 90-day written notice of resignation in January.

Communication Strategy

All 683 patients attributed to that plan received a personalized letter six weeks before the effective resignation date, followed by a phone call from a trained front-desk team member. The letter explained the change, offered to verify alternative insurance coverage, and emphasized the practice’s commitment to continued care. Patients were offered a one-time complimentary exam visit for those choosing to remain as out-of-network or self-pay patients.

Results (18-Month Follow-Up)

- Patient retention: 74% of affected patients remained active after 12 months

- Revenue impact — Month 6: Net collections declined 11% from baseline

- Revenue impact — Month 12: Net collections returned to 98% of pre-resignation baseline

- Revenue impact — Month 18: Net collections exceeded pre-resignation baseline by 16%, driven by full UCR billing on retained patients and new FFS patient acquisition

- Write-off reduction: Total annual write-offs declined from $218,000 to $134,000

The critical insight from this case: the initial revenue dip was shallower than projected, and recovery was faster. The practice had underestimated how many patients would stay simply because they valued the relationship with their dentist.

Case Study 2: The Two-Doctor Group Practice That Resigned Three Plans Simultaneously

Background

A two-dentist group practice in a competitive suburban market, approximately 3,400 active patients, credentialed with nine PPO plans. Three plans — all subsidiaries of the same parent carrier following a regional acquisition — were paying nearly identical, below-market rates and collectively representing 51% of gross production with a 47% average write-off rate.

The Decision

The practice engaged a dental-specific consulting firm to model the attrition scenario before resigning. The model projected 55–65% patient retention across the three plans’ combined patient panel of 1,740 patients. The practice chose to resign all three simultaneously to execute a single, unified communication campaign rather than three separate transition periods over 18 months.

Communication Strategy

The practice sent a tiered communication sequence: letter at 8 weeks, personalized phone call at 6 weeks, follow-up letter at 3 weeks, and a courtesy reminder call at 2 weeks. The messaging was transparent — “We are no longer in-network with [Carrier], but we want to help you understand your options and continue your care here.” The practice also launched an in-house membership plan simultaneously, giving uninsured and affected PPO patients an immediate alternative.

Results (24-Month Follow-Up)

- Patient retention: 61% of affected patients remained active — slightly below the conservative end of the projection

- Revenue impact — Month 9: Net collections declined 18% from baseline (the most significant dip in any case study here)

- Revenue impact — Month 15: Net collections recovered to 94% of baseline

- Revenue impact — Month 24: Net collections exceeded baseline by 22%

- In-house plan enrollment: 287 patients enrolled in the membership plan within the first 6 months

- Write-off reduction: Total annual write-offs declined from $487,000 to $241,000

The simultaneous resignation created a deeper short-term revenue dip than a phased approach would have. However, the group reached full recovery faster because they could focus all new-patient marketing on FFS and membership-plan prospects simultaneously, rather than running parallel campaigns. Dental Economics has reported similar findings in multi-site transition analyses — phased approaches carry lower peak risk but slower recovery arcs (Dental Economics, 2024).

Case Study 3: The Specialty-Adjacent Practice That Used PPO Resignation to Reposition

Background

A general dentist with advanced training in implant placement and full-arch restoration, practicing in a urban market. The practice had a strong implant volume but was credentialed with four PPOs, none of which covered implants. The PPO patients consumed significant chair time for basic restorative work at heavily discounted rates, crowding out implant cases — which were exclusively fee-for-service — from the schedule.

The Decision

This case is distinct because the motivation wasn’t purely financial. The primary driver was schedule optimization: the dentist wanted to increase implant case volume, which required reducing the chair-time demand from low-margin PPO restorative patients. After mapping the opportunity cost (the number of implant cases that could replace a full day of PPO crown work), the decision to resign two of the four PPOs was straightforward.

Communication Strategy

Patient communication emphasized continuity: affected patients were informed of the network change and offered referrals to nearby in-network providers for their routine restorative needs, while being explicitly invited to remain for any implant, cosmetic, or complex restorative needs. The practice positioned itself honestly as a provider focused on advanced restorative care.

Results (12-Month Follow-Up)

- Patient retention for routine restorative: 42% — lower than other cases, but aligned with the practice’s intent to transition those patients

- Implant case volume: Increased 68% within 12 months as chair time opened

- Average production per day: Increased from $4,200 to $6,800

- Net collections: Increased 31% year-over-year despite lower active patient count

This case illustrates a point that pure retention statistics can obscure: not all patient attrition is failure. When a practice deliberately repositions toward higher-value services, some attrition is the intended outcome. Revenue per patient, production per day, and net collections are the metrics that matter.

What Patterns Emerge Across All Three Cases?

Several consistent findings cut across all three transitions:

- Patient retention consistently exceeded pre-transition fears. In every case, the dentist’s initial gut estimate of likely attrition was more pessimistic than actual outcomes.

- Communication quality was the single most controllable retention variable. Practices with multi-touch, personalized communication protocols retained significantly more patients than those relying on a single form letter.

- Recovery timelines ranged from 12–18 months for single-plan resignations to 15–24 months for multi-plan simultaneous transitions. These timelines are predictable and plannable.

- In-house membership plans materially accelerated recovery by capturing resigned-plan patients who chose to stay but lacked alternative coverage.

- Post-transition revenue exceeded pre-transition revenue in all three cases — not despite the attrition, but partly because of it, as the remaining patient panel was billed at UCR rates and mix-shifted toward higher-value treatment.

For the full strategic framework underlying these transitions, see our pillar guide: Reducing Insurance Dependency in Dental Practices.

If you’re earlier in the process — still assessing whether to negotiate before resigning — read our detailed playbook on how to negotiate better dental insurance reimbursement rates. And for the financial planning that should precede any transition, our guide on financial stability after dropping PPO plans covers the reserve requirements and cash flow modeling you’ll need.

Last Updated: March 2026