The first year after resigning from a PPO plan is financially predictable — if you’ve done the planning work in advance. Practices that enter the post-PPO period with accurate cash flow projections, adequate reserves, and a structured patient communication plan find the transition manageable. Practices that don’t are exposed to a revenue gap that can take two or three years to close rather than one. This guide maps the 12-month financial timeline you should expect after dropping a PPO plan, with patient retention curves, revenue recovery patterns, and reserve requirements based on documented practice outcomes.

What Does the First 90 Days Look Like Financially?

The first quarter after PPO resignation is the most financially volatile period. Revenue from the resigned plan’s patient panel declines sharply as some patients follow their insurance to another in-network provider. At the same time, your overhead structure hasn’t changed — staff costs, facility costs, and lab fees remain constant regardless of patient volume.

For related reading, see our guide on negotiating better dental insurance rates.

The typical net collections decline in months 1–3 ranges from 8–20% below pre-resignation baseline, depending on how large the resigned plan’s contribution was and how many patients transition out. For practices where the resigned plan represented 25–30% of gross production, the dip lands toward the higher end of that range.

The American Dental Association’s Health Policy Institute notes that practices that execute a formal patient communication protocol retain significantly more patients through the transition period than those that rely on passive notification (ADA Health Policy Institute, 2023). Every percentage point of additional patient retention directly shortens the recovery timeline.

The Cash Reserve Requirement

Before resigning any PPO, you need liquid reserves equal to 3–6 months of your practice’s fixed overhead. Fixed overhead — the costs you incur whether or not you see patients — typically includes debt service, staff salaries, lease payments, and insurance premiums. For a practice with $55,000 in monthly fixed overhead, that means $165,000–$330,000 in accessible cash before you file the resignation letter.

This is not a conservative recommendation — it’s the floor. Practices that enter a PPO transition with less than two months of fixed overhead in reserve face the compounding pressure of a revenue dip and a potential credit crunch simultaneously.

How Does Patient Retention Typically Curve Over 12 Months?

Patient retention following a PPO resignation doesn’t follow a linear decline. It follows a curve that front-loads the attrition. Here’s the general shape documented across multiple practice transitions:

Months 1–2: The sharpest attrition period. Patients who prioritize insurance network membership over provider relationship depart during this window. These tend to be patients with lower treatment complexity, less tenure with the practice, and more price-sensitive dental decision-making. Expect 15–30% of the affected plan’s patient panel to leave during this period.

Months 3–6: Attrition slows substantially. Patients who stayed through the initial transition are demonstrating a degree of loyalty. Some additional departure occurs as patients’ annual benefit periods reset and they seek in-network providers. An additional 5–10% attrition is typical in this window.

Months 7–12: Attrition approaches zero. Patients still active at the six-month mark have effectively decided to remain with your practice regardless of network status. In most documented transitions, fewer than 2% of remaining patients leave in the back half of the first year.

The composite result: a practice that communicated effectively and executed the transition well typically retains 60–78% of its affected patient panel after 12 months. That retention rate, applied to UCR fees rather than PPO write-down rates, drives the revenue recovery math.

What Is the Revenue Recovery Timeline?

Revenue recovery follows the patient retention curve, but with an important modifier: per-patient revenue typically increases post-transition for retained patients, because those patients are now billed at UCR rates rather than the discounted PPO schedule.

A practice that retained 70% of its affected patient panel at UCR fees will generate more revenue from those 70% than it generated from 100% at PPO rates — provided the PPO write-off rate was 30% or more. The break-even math is straightforward:

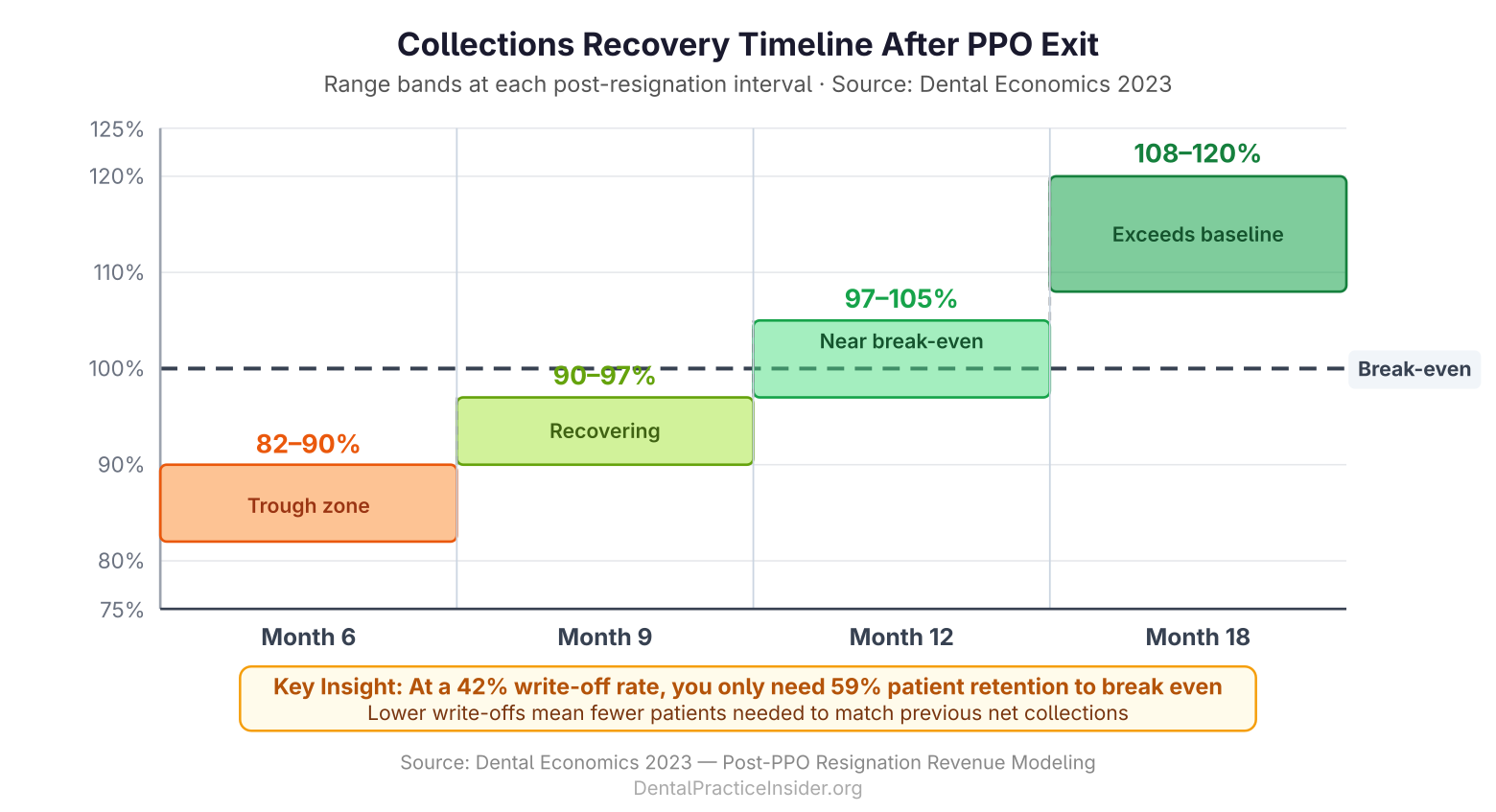

If a PPO was paying 58 cents on the dollar (a 42% write-off rate), retaining just 59% of affected patients at full UCR generates equivalent gross revenue. Everything above 59% retention is net improvement.

The recovery pattern published in Dental Economics for single-plan resignations shows:

- Month 6: Collections at 82–90% of pre-resignation baseline

- Month 9: Collections at 90–97% of baseline

- Month 12: Collections at 97–105% of baseline

- Month 18: Collections at 108–120% of baseline

The 18-month figure exceeding baseline reflects both the UCR fee benefit on retained patients and the practice’s ability to attract new fee-for-service patients into the appointment slots previously consumed by high-volume, low-margin PPO work.

What Operational Changes Drive Faster Recovery?

Practices that recover fastest after PPO resignation aren’t just waiting for the math to resolve — they’re actively managing four levers simultaneously.

Increase New Patient Acquisition

Every appointment slot vacated by a departing PPO patient is an opportunity to replace a write-down patient with a full-fee patient. Increasing new patient flow through targeted marketing, referral programs, and Google Business Profile optimization directly accelerates recovery. The unit economics are straightforward: one new FFS patient generating $1,200 in annual production replaces the contribution of two or three mid-range PPO patients after write-offs.

Launch or Optimize an In-House Membership Plan

An in-house membership plan captures patients who want cost certainty without the administrative friction of traditional insurance. These plans — typically priced at $25–$40/month or $300–$480 annually — provide predictable, pre-paid revenue and often carry higher treatment acceptance rates than traditional insurance patients. See our guide on benefits of in-house dental plans for structure and pricing details.

Reactivate Dormant Patients

Most practices have 15–25% of their patient database in a dormant state — patients who haven’t been seen in 18 months or more. A structured reactivation campaign targeting these patients can generate appointment volume without new patient acquisition costs. Many dormant patients have unmet treatment needs and will convert at higher acceptance rates than new patients because they already trust the practice.

Optimize Treatment Presentation

Post-PPO practices often experience improved case acceptance because the fee conversation becomes simpler. Without the complexity of insurance coverage limitations, pre-authorizations, and benefit caps, treatment planning and financial discussions are more transparent. Training the team on value-based fee presentation accelerates case acceptance in the post-PPO environment.

What Are the Longer-Term Financial Outcomes?

The 24–36 month picture for practices that have successfully navigated a PPO resignation is consistently positive in documented outcomes. The structural reasons are not complicated:

- Write-offs are permanently reduced for the resigned plan’s former patient panel

- Per-patient revenue is higher for retained patients billed at UCR

- Administrative costs decline — fewer claim submissions, fewer downgrades to adjudicate, fewer coordination of benefits disputes

- Cash flow improves — fee-for-service and membership plan revenue is collected at point of service rather than waiting 30–90 days for carrier remittance

- Overhead as a percentage of collections typically declines as revenue grows without proportional cost increases

Practices that complete a full PPO risk reduction program — resigning their lowest-value plans, renegotiating remaining contracts, and building in-house membership plan revenue — routinely report 15–25% improvements in net income per dentist over a 3-year period. That outcome reflects the compounding effect of all the above factors working together.

What Are the Warning Signs That a Transition Is Going Wrong?

Not every PPO transition proceeds smoothly. The warning signs that a recovery may be stalling include:

- Patient retention below 50% at month 3 — suggests communication strategy or patient relationship gaps that need immediate attention

- New patient flow flat or declining — means the replacement patient strategy isn’t working and needs a marketing intervention

- Collections still below 85% of baseline at month 9 — may indicate the practice needs to re-evaluate remaining PPO contracts or accelerate membership plan growth

- Team turnover during the transition — front desk and hygiene team stability is critical to patient retention; staff uncertainty about the practice’s direction can directly drive patient attrition

If any of these warning signs appear, the appropriate response is diagnosis and targeted intervention — not reverting to the resigned PPO. Re-credentialing typically takes 90–180 days, and the underlying financial problems that prompted the resignation still exist.

For the complete framework on building long-term insurance independence, see our pillar guide: Reducing Insurance Dependency in Dental Practices.

If you’re still in the planning phase, our PPO risk management guide covers the audit and analysis work that should precede any resignation decision. And for real-world precedent on what these transitions look like across different practice types, see Dental PPO Transition Success Stories.

Last Updated: March 2026

For more resources on this topic, see our complete guide to insurance independence strategies.